(5 min read)

Millennials have become the largest population in the US.

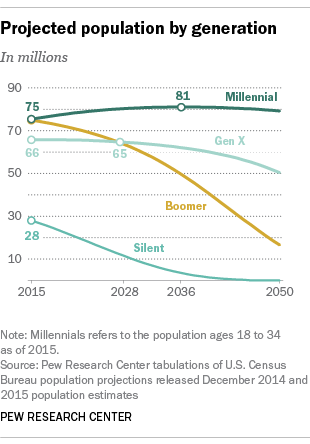

Millennials (those born in between 1981 and 1998) are now the America’s largest generation, overtaking the baby boomers, according to Pew Research Center.

Not only are they the largest age demographic, but they may soon be, if are not already, the richest. As the economists call it, the “Great Wealth Transfer” has officially begun. The millennials are “inheriting roughly $30 trillion in assets from their aging parents and grand-parents.”

30 trillion dollars. That is 1.6 times the annual US GDP, according to the World Bank. Accordingly, the massive migration of assets is expected to have a tremendous impact in every sector, including the finance and fintech industries.

To better understand the impact of this massive transfer on financial service providers, we want to dive deeper into millennials’ major life milestones, which are hugely tied to significant financial decisions, such as buying a house.

How millennials make different choices

(And quick takeaways for financial providers)

1. On mortgages

In the past three years, millennials have become the largest source of new mortgage originations, according to American Banker.

And they seem to be more satisfied with their lenders than older generations have been, according to J.D. Power Satisfaction Study. Interestingly, the reason for such satisfaction comes from improved services on “communication, both via digital and via interpersonal contact with loan representatives.”

Take away> This means that mortgage lenders who want to stay competitive need to have customer communications that meet or beat updated expectations.

2. On owning a home

Although millennials are the largest source of new mortgage originations , homeowners still only make up a small fraction of the whole Millennial population.

When compared to the older generations, millennials don’t buy homes like others used to. The percentage of millennials owning a home fell to the lowest level since 1965, according to the CNBC.

The trend is bifurcated. Some are deferring home purchase, where as others can’t simply afford to buy a house.

The home deferrers are mostly ambitious, well-educated millennials who are super mobile, moving out for college, settling in an urban city, deferring marriage, and, hence, deferring buying homes.

On the other hand, the remaining millennials who are less mobile - who live in similar neighborhoods to those that they were born into - remain in the same region that their parents and grandparents are living in, and often end up failing to buy homes.

Takeaway> This means that financial service providers will have to look to provide non-mortgage related services in order to develop earlier, meaningful relationships with home deferrers, and may need to rethink their approach to less mobile young people all together.

3. On using credit cards

According to the New York Times, “the percentage of millennials who hold credit card debt has fallen to its lowest level since 1989,” while the household debt in the United States escalated to $12.29 trillion (2Q 2016).

Millennials prefer to opt in for debit cards, apps like Venmo or Apple Pay, which draw funds directly from a bank account.

Why? Many attribute this avoidance of revolving credit to soaring education burdens. With average American under 35 having $17,200 student loan debt, many are waiting to expand their credit.

Takeaway> Successful financial services firms will create new products that help students build financial confidence while managing high-levels of debt early in their lives. They could focus on products that increase productivity or reduce the risks associated with income instability.

4. On getting married

Millennials aren’t only differing from previous generations on the timing of their marriages, but also often choosing not to get married at all, says Science Daily.

Psychologist Antonia Hall says millennials are “less likely to buy into marriage” as a result of being raised with rising divorce rates and broken homes.

She adds that increasing educational costs and related debt push millennials to feel less financially secure. Also, cultural shifts are happening as well, from Tinder’s hookup culture to open relationships, expanding views on what partnerships look like.

Takeaway> For families this often means that important conversations about finances, insurance, and responsible decision making that have traditionally accompanied marriage, home-buying, or the birth of a child are now occurring much later or not at all in many cases.

Financial services who step in earlier to help younger singles understand these important steps as they reach adulthood are set to benefit from stronger relationships with their customers when they finally to take those next steps.

In summary, a minority of millennials have become the largest mortgage originators, but most of them aren’t buying homes, aren’t using credit cards, and aren’t getting married, as the older generations used to.

This all boils down to the following question:

“How would financial service providers innovate their offerings – products, distribution channels, marketing – to better serve the millennial who have different set of needs and priorities?”

Quesnay has been focused on helping traditional firms answer this question for more than 5 years, bringing together the most innovative ideas and talent through innovation competitions, creating and maintaining engaging touch points with millennials by forging digital partnerships, and preparing to launch a fintech startup competition in Q3 of 2017. (More on fintech startup competition later!)

We’ll continue to explore the topic of fintech, digitization, and millennials in the coming months. Meanwhile, we’d love to hear your thoughts and comments, so leave a comment below to continue the discussion or write us an email!

How is your organization, business unit, or start up responding to the great wealth transfer?

Image and icons coursety of blog.emoneyadvisor.com and flaticon.com